REAL ESTATE INVESTMENT: Qualified Opportunity Zone Fund

Great news. The Qualified Opportunity Zone Fund Program (OZ 2.0) is now permanent and better than ever. If you’re sitting on capital gains (or 1231 gains), this program will let you defer and/or entirely eliminate federal taxes from qualifying investments.

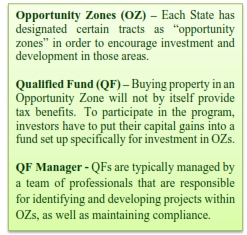

The Opportunity Zone program has been around since 2017 but, since the Pandemic, it has received some nice tweaks you should know about.

Benefits

When trying to understand the ins and outs of the program, the first thing you need to understand is that we’re really talking about TWO separate taxable amounts. Let’s call them GAIN #1 and GAIN #2.

GAIN #1 – Previous Capital Gains

Here, we’re talking about the capital gains you have already realized.

If you’re just sitting on this money at the moment, getting ready to pay taxes on it, hold on. There is an alternative.

What you can do instead is take those gains and reinvest them in a Qualified Opportunity Zone Fund («QF» for short). That will exempt those gains from this year’s tax return. The bill will come due, but you get to defer the payment. Stay with me.

Example: Let’s say you sold real property last year and made a profit of $500,000. For the sake of this example, say you owe 20% in capital gains tax on that money, which would be $100,000. Under the OZ program, Uncle Sam basically says:

You can hold onto my $100,000 as long as you reinvest it in an Opportunity Zone. And, I’m going to give you 180 days to find the QF you like and make the investment.

That is not a bad deal, but you’re going to want to wait until after January 1, 2027. If you do, then _

you will get a 5-year «rolling» deferral AND a discount on the tax (step up in basis)

After a five-year holding period, you get a 10% step-up in basis with a regular OZ. If you’re willing to do a Qualified Rural Opportunity Fund, you get a 30% step up in basis after the same five years.

Come on now. That’s some sweet action. But, there’s much more …

GAIN #2 – Capital Gains from Qualifying Opportunity Zone Fund

So, Gain #1 is the money you made on a past investment. You will get some nice tax breaks on that through the OZ program, but now let’s look at Gain #2. That’s money you make on your investment in the QF. This is where things get crazy.

Continuing with our example, if you leave your $100,000 investment in the QF for at least 10 years, you’re going to get all the capital gains derived from that investment TAX FREE. Let that sink in.

Example: Let’s say you find a good QF for your $100,000. You can probably expect your Fund Manager to grow the fund at a rate of 10% to 15% per year. That will essentially double your investment in five (5) years. So, by year five, give or take, your $100,000 investment will have grown to $200,000. And, by year ten (10), it will be worth $300,000. That leaves you with a capital gain of $200,000 by the end of the 10-year cycle.

Guess what. You will pay exactly zero taxes on that $200,000 gain.

That, my friends, is rather amazing.

Now that we have your attention, look for follow up articles with details on _

- Who can invest in a QF?

- What kind of money qualifies for a QF?

- What kind of projects are in an Opportunity Zone?

- What is the risk analysis for a QF?

- How does a QF compare with a 1031 Exchange?

- Where do I find a QF to invest in?